The Investing Meta-Game

“Over the last decade, I’ve interviewed and assessed more than 5,000 investment managers. One of the most important things I’ve learned in that process is what separates the great investors from the rest. The great ones view investing as a game, and they know exactly what game they’re playing”

– “The Playing Field”, Graham Duncan, Eastrock Capital

Last month I read the Chinese science fiction book The Three-Body Problem: in a virtual world, the protagonist is challenged by inconsistent cycles of day and night which are unexplained until he realizes there are three planetary bodies: the Earth, and two suns. In this story, the “third body” exerts an unseen force distorting the gravitational relationship between the Earth and the Sun. The wonderful thing about science fiction is it forces the reader to consider the world unbounded by the thinking of habit: the air we breathe or the water we swim in. The goal of this essay is to “re-frame” investing in a way that might allow us to see the deeper investing meta-game, or the game within the game.

This essay explores, through the metaphor of the “The Water We Swim In”, why changes in the market environment are changing the investment strategies that may work going forward.

There are five important takeaways:

All investors are engaged in a common myth – or narrative;

Most investors describe the “quality” of their investment process, but this is only one part of what generates alpha; it is investment process relative to your competition which matters more;

A strategy’s ability to generate alpha (or excess return) depends on the eco-system in which it operates. And most investment alpha can only be generated relative to another dominant strategy;

All investment strategies, even value investing, are information front-running. Widely available information reduces these opportunities;

Idiosyncratic risk is likely the last preserve of human investment managers?

A Discounted Cash Flow is but one “narrative” of the value of a company

Most investors, myself included, take some intellectual comfort from the view that we are investing based on discounted cash flows (“DCF”), however we choose to define them whether DCF, or its shorthand derivations, P/E, EV/EBITDA, etc.

Yet many companies today have an average expected corporate life shorter than the DCF used to value them: in most DCF’s, terminal value is the most important driver. As a result, what we believe today about the future is unlikely to be true, and investors almost never achieve the “modeled” return. DCF-investing works because most other investors also believe, or will eventually, that a DCF is a reasonable measure of fair value for a company. Investors deal in relative, not absolute truths. There are of course some exceptions (such as arbitrage, deep value with high earnings / dividend yields, etc)

Investors then are dealing in a “DCF narrative”, the same way all societies share beliefs about the intangible qualities of money. And sometimes these narratives change, as we described in The Investment Paradox of Software, investing seemed to move from the tribe of the Benjamin Graham net-net to tribe of Buffett / Munger See’s Candy reinvestment moats, with tremendous benefits to those who recognized it first. Other times these narratives collapse – usually following being proved wrong – like the 1950’s conglomerate boom.

Why alpha is a relative game

Most investors understand alpha as the excess return an investor earns above his / her portfolio’s beta- or factor-returns. But alpha can be imagined differently, as the return extracted from other market participants, understood through the analogy of a parasite:

“the most effective alpha-generating investment strategies are parasites … [which] uses the market itself as its habitat. It’s not an investment strategy based on the fundamentals of this company or that company – the equivalent of a geographic habitat – but on [exploiting] the behaviors of market participants [behaving for non-economic or institutionally-caused biases]. A parasitic strategy isn’t the only way to generate alpha – but I believe that the investment strategies with the largest and most consistent “edge” are, in a very real sense, parasites.”

– Parasite Rex, Epsilon Theory

Simplified examples can yield important insights: a horse-race is a close analogue to the stock market.

Two variables determine successful bets. First, you must have some foresight in the future through betting on the right horses: this is an “investment process”. Second, you must also identify where the odds, implied by prices, are different than your view of the future. For example, a bet on Sea Biscuit in the 1938 Kentucky Derby merely identifies what the crowd already knows, and prices reflect such. The stock market is similar: investors bet on future company profitability relative to stock valuations (price-earnings ratio, for instance). Most investors understand this.

There’s one more important point. Imagine you have an “investment process”, in this case you collect statistical data on past horse races to forecast the future. You address your behavioral biases. You have “long-term capital”, which means you’re betting with your own money. Yet, after years of betting, your results are statistically no better than average.

At this point, the poor bettor probably reflects on his results, revisits his “process” and sees no obvious reason for his underperformance besides the fact that maybe luck runs in streaks and his approach is “out of favor”. He’s missed an important point, its not the sophistication of his process that matters, it’s the quality of his process relative to the pool of competitors -- and likely his pool of competitors has changed. Thus, it may not matter that your team does pre-mortem reviews, red-team / blue-team, checklists, or any of the like, as the incremental quality of decision-making does not overcome a very real problem: most of your competitors are doing it too.

In this respect the parasite analogy is astute. Parasites (strategies) can only survive in the presence of an available host (counterparty), the same way a value strategy can only survive against market participants which set prices under other (non-fundamental) considerations. And as of today, there are 40,000 “contrarians” attending the Berkshire Hathaway meeting, chances are in most stocks you traffic, the person selling to you is the “contrarian” sitting in the bleacher seat next to you. You are trading against you, with each person believing that the person selling to them is behaviorally defective, analytically deficient, and mostly devoid of the information necessary to calculate a price-earnings multiple.

All value investing is information front-running within a dominant narrative

“The only way to make money reliably on Wall Street is by front running. Front running means to buy or sell things ahead of others, knowing or expecting that other people will follow you later. Short term front running is often called ‘illegal’. Long term front running is often called ‘investing’.”

– Thomas Peterffy, Founder, Interactive Brokers

Is value investing also information front-running? … I think it is. A successful value investment goes something like this: one buys a stock at a P/E multiple of 6x, holds for a few years during which EPS grows and dividends are paid, then sells the stock at a P/E multiple of 10x. Our value investor makes money from some combination of predicting the future, buying at a cheap price, then having the market (others) agree with him. Very few investors hold a stock for the duration of their DCF forecast.

Value investors are front-running, the same way momentum investors do, the same way scalpers do in an open-outcry pit: we assume some special insight the market has failed to recognize.

We can now recast the hedge fund investing game. Consider the small cap value manager of 1990. Sitting in an office with a rented Bloomberg terminal, he had access to more financial information, available instantaneously, than any previous investor in history. Technology took something scarce (financial information, access & attention) and made it more abundant.

The manager, discovering a $500M small-cap stock trading below book value at a 6x P/E was certainly quite the find. He purchased the stock, collected a very high earnings / dividend yield, and waited. His high return was realized when another value investor discovered that same stock, thinking it must be worth 10x P/E, and paid him a handsome profit. Conversely, it could also be the case that the stock formerly sold at 10x P/E, was sold down, perhaps due to a forced sale, to 6x P/E, and then picked up by the value investor. In either case, the investor was trading against another participant in the stock market and had to be at least partially right, if earnings collapsed in the interim the math wouldn’t work. And time was an accelerant.

Reading the early Greenlight or Tiger Management letters during their heyday, one realizes it was not rocket science, and the hurdle was low, but they were first. The Ivy League graduate sitting in front of the most amazing information machine the world had ever seen, simply had to be marginally brighter than the mom & pop he was buying from. And in those days, it was mostly mom & pop’s he was buying from in the small-to-mid cap space.

Recast in this light, hedge funds were at the leading edge of an information revolution when Bloomberg took the lever of technology to solve a very acute problem: the non-scalability of human attention. This is a fancy way of saying there were more orphaned, undiscovered small-cap stocks available than qualified investment analysts to physically unearth them, whether due to limits of attention or geographic fragmentation (access to reports, management, or information about the business).

What is interesting is we are not describing an “investing” problem per-se, we are really describing an information-problem:

"Perhaps the most enthusiastic proponent of an information-based theory of physics was Edward Fredkin, who in the early 1980's proposed what he called a new theory of physics based on the idea that the Universe was comprised ultimately of software. We should not think of ultimate reality as particles and forces, according to Fredkin, but rather as bits of data modified according to computation rules."

– "Reflections on Stephen Wolfram's A New Kind of Science", Ray Kurzweil, May 2012.

Yet many business moats we consider to be problems of position or proximity, like real estate brokers in New York, who take 15% cut of annual rents, can be described (and solved) as information-problems. How many apartments would you have to see if you knew instantly through virtual reality what was available and what each apartment looked like? Would you still pay your broker 15%?

In other words, physical location was a proxy for information: a real estate broker’s service can almost be completely described to you in information that flashes across a screen. We think photos are analog and information are things that fit within Excel spreadsheets, yet that is not quite true. Information is more than that, but for most of our lives we lacked the technological tools to describe these analog inputs in a digital medium. Re-framing business problems as information-problems allows one to create equivalence between investment concepts we understood in a physical sense and their digital equivalents.

For example, if you believe this analogy, then companies like Google are really the Goldman Prop desks of the information age. Proprietary trading desks made money by harvesting the flow of trading information coming across their desk, taking a spread between buyer and seller. Most times you search on Google, you are a buyer (of information) in search of a seller, and Google sits in the middle, replacing the function of advertising, but also of real estate. Different properties like search, Youtube, Maps, Gmail, or Android are merely the town squares of the virtual world where buyers and sellers congregate to transact. Each search query is a bustling main street built in a virtual world just for you with Google taking a spread between information buyer and seller. Goldman Sachs monetizes this spread by taking a percent of dollars transacted, Google monetizes this spread by selling someone else the right to give you a bit more information about their product as well.

What ultimately may be true is many businesses at their core revolve around information facilitation: consumer brands convey quality information, capital markets convey asset & cash-flow information, sales executives convey customer information, real estate brokers convey location information, and distribution conveys price / availability information. If you are looking for some underlying truth that broadly explains the disruption occurring, it may be this: the marginal cost of acquiring information has plummeted.

“What important truth do very few people agree with you on?”

– "From Zero to One", Peter Thiel

In our analogy, one explanation is the hedge fund manager was merely the beneficiary of being on the leading-edge of commoditizing financial information. He was a first-mover of the “value investor tribe” invading the habitat, and there were plenty of value investors coming after him who would be willing to pay more. By luck, hard work, and access to information, he was the first to “discover” that cheap stock hiding in plain-sight, and for most of the 1990’s made 20%+ returns everywhere, almost irrespective of whether the overall market was up or down. As cash continued to pour into these strategies, popularity begat popularity, and the only thing better than a “undiscovered” stock at 6x P/E was the next value-investor following you in. The business could ultimately be worth zero, but the investor could sell to someone else at 10x P/E long before that transpired. That trend seemed to stop around 2014.

Thus restated, investment alpha is the collection of informational insights which is currently in the minority, but likely to become the majority. You can’t have a non-correlated alpha-abundant return stream unless you have these types of “parasitic” conditions:

This was the water value investors were swimming in, yet we never knew it. Like the Jack Schwager Market Wizards books of the 1990’s where every successful trader looked like some rare combination of divine insight or talent, "any sufficiently advanced technology is indistinguishable from magic". And at its core, what these traders had was access some of the best information tools the world had ever seen, not because they had more resources at the time, but because they were there when they became available. As we better understand technology, information and the role it plays in stock markets, we begin to defuse the aura of magic into one of limited opportunity.

The stock market and the Bloomberg terminal were merely the stratum and the technology allowing a few individuals to extract large amounts of money from the value of newly available information. Today those same trends are playing out in a much larger arena where Facebook and Google are the Bloomberg terminals of the physical world, and their founders are worth more than the last generation of information brokers, the investment bank CEO.

The Water We Swim In: The stock market eco-system of today

“One game that is currently operative among many skilled investors is buying quality companies in the midst of short-term difficulties … But a game like this will likely work for several years, before it becomes such a common approach that these “quality” stocks will become less volatile during periods of stress (many high-quality consumer stocks in Asia currently seem immune to sell-offs based on macro uncertainty). So an investor who uses only one game will have less sustainable returns than those who reach the next stage: putting in the time to develop new games even while playing the existing one.”

– “The Playing Field”, Graham Duncan, Eastrock Capital

One mentor in the investing game came from the index-arbitrage / program trading desks of the 1990’s, who themselves were manifestations of being the leading edge of commoditizing information. I once asked him how he knew when to buy a stock and he said it was when the stock no longer went down on bad news – bad news was already in the price.

What both stories illustrate, through the proxy of market price, was the composition of other investors in the stocks we swim in. The implications are profound.

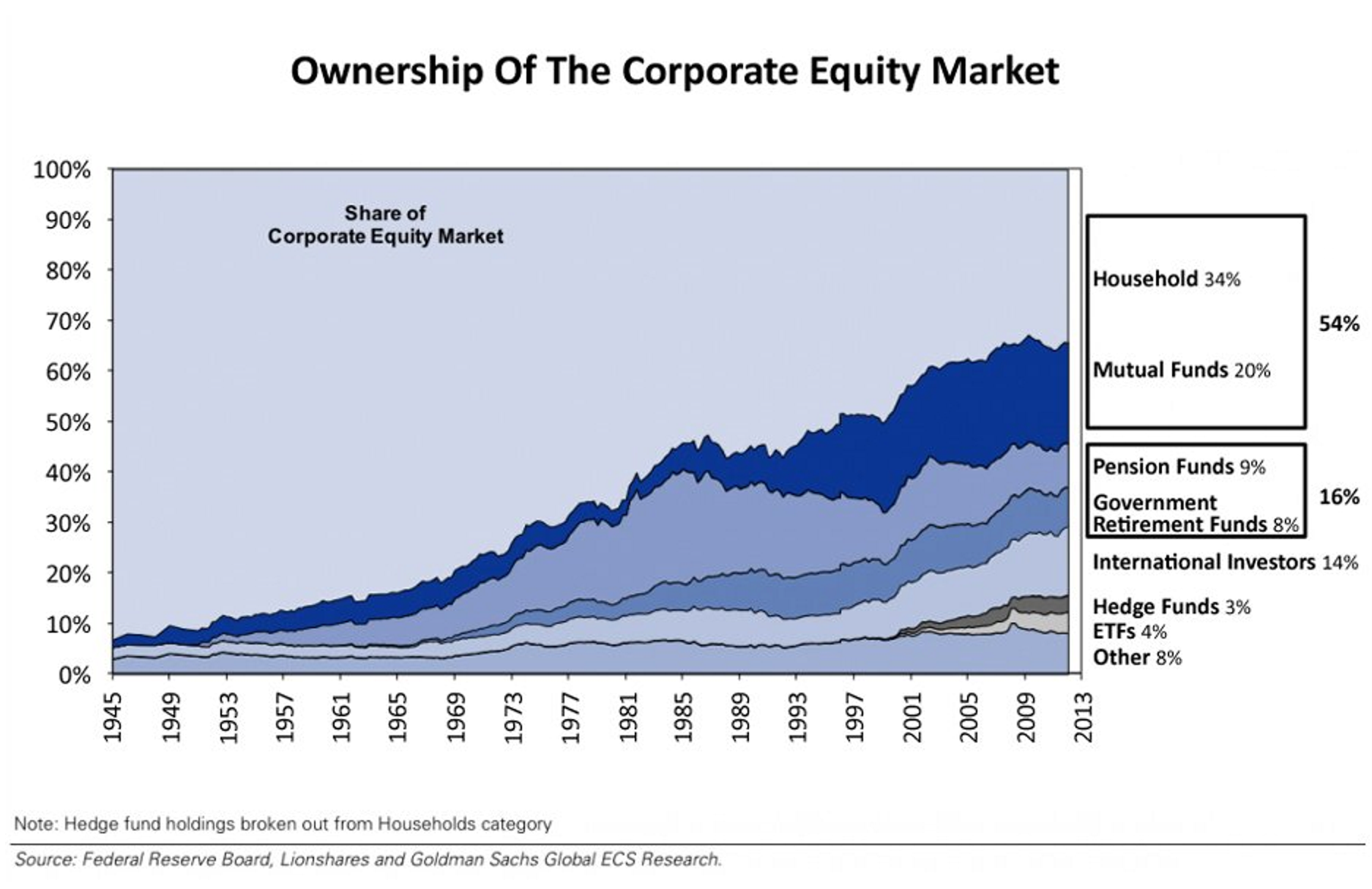

Today’s habitat is dominated to a large extent by machines. Their investment processes derive signals and operate in the world of probabilities. These programs don’t necessarily sell when they face a 20% drawdown nor are they limited by the eight-hours in a day to hunt for new ideas. Machines can be everywhere at once provided data-sets exist for the signal in question. They can be in small cap stocks with limited analyst coverage or frontier markets where they can only take 10 basis point positions, in fact many of them hold >3,500 stocks across the liquidity spectrum. And the presence of these participants changes the investing-game you’re playing. Quant strategies may not incorporate many intuitive judgements, but in some ways they don’t have to, their mere presence can in aggregate drastically effect the prices (odds) available.

In fact, most “quality” ETF’s today are almost indistinguishable from the “long compounder” books of most hedge and mutual funds. Human managers may have additional insights, but if those insights leave them with the same portfolio as one constructed using a set of signals, performance is almost guaranteed to be indistinguishable, especially where long-term holdings are concerned. Fund managers can add a few additional points of return by trading around the volatility, but it’s not the same reflexive return drivers we've described which existed in the 1990’s.

Furthermore, if you are doubtful whether a computer can account for complex intuitive judgements, the reality is humans aren’t that good at it either. As Andrew Haldane, the Chief Economist of the Bank of England quipped in a recent speech, the perfect physics solution to a frisbee-catching dog is to calculate the speed, angle of ascent, wind speed, rotations per second, etc. Yet for all that complexity, a dog following the simple rule of thumb of looking up, keeping its eye on the frisbee, and running in the same direction works much better.

Simple heuristics for central bank policy-making work much better than most econometric models when predicting complex phenomenon. When the simple outperforms the complex, it implies there are limits to what we can know about the future. The inability of most investment managers to beat their factors, or the index, suggests that in the current eco-system and its participants, simple rules may work better than complex ones for many (but not all) investment problems.

The irony is the biggest inefficiency of stock markets is not the inability to do a Discounted Cash Flow (DCF) model, or its equivalents, the biggest inefficiency is the human in ourselves. And most stock market strategies at their heart are parasitic exploitations of the inefficiencies of other human participants. The implication of the shifting market eco-system from human-to-machine participants means many strategies depend on implicitly assumed conditions of the habitat that may no longer be true.

Idiosyncratic risk: the last preserve of human investment managers?

“David Harding (Winton Capital, a famous quant fund) has told colleagues that Buffett gets his investing "edge" by knowing everything about everything. By contrast, Harding applies statistics and technology to provide some degree of certainty to markets that are inherently uncertain.”

– Winton Capital Founder David Harding on Artificial Intelligence - Barron's

In poker, which has similar dynamics to horse-race betting, the optimal strategy depends on other players. This is true in the stock market as well. There are always opportunities to outperform in stock markets but the best strategy depends against whom the game is played.

The eco-system of today is different from the one Warren Buffett inhabited in 1950’s when he was competing against mom & pop retail investors. Or even the habitat Bill Miller faced in the 1990’s when he described his investment edge as “informational, analytical, and behavioral”.

If the stock market is an eco-system and a successful alpha-generating strategy is one that trades against the dominant biases of others, what are the now dominant biases?

It seems the best way to approach such a question is to make a guess as to what the dominant strategies are today: such as passive indexation, valuation dispersion (multi-manager strategies arbitraging different relative valuations within sectors), and fundamental quant-strategies, then infer what their dominant biases might be:

Passive indexation: largely market-cap weighted indexes with an inbuilt bias that big companies get bigger. These strategies would miss situations where market breadth became very narrow, or a regime shift.

Valuation dispersion: valuations within sectors are correct but across sectors could be wrong?

Quant-strategies: many statistically cheap oriented value strategies such as small-cap or EM investing might be crowded relative to their capacity. Strategies relying on pricing and extrapolating past historical trends would also be well-priced, such as high ROE’s.

If true, where would active managers of the DCF-tribe find opportunity?

Compounders, a non-parasitic market game: these work based on a very simple premise: they are most resistant to the efficiency of stock prices as their returns are determined by the incremental re-investment rate and not their entry-valuation. A compounder bought at 15x P/E is a better investment than one bought at 25x P/E, but in the end, the compounded annual return of both will converge to the business reinvestment rate over a long enough time frame. Stated another way, the popularity of “compounder” strategies may be tacit acknowledgement of the lack of opportunity in more parasitic investment strategies relying on information asymmetries.

Many institutional market participants today have mandated limits on portfolio concentration (and so do index products): they are forced sellers of large behemoths even when the prospects remain compelling. The danger comes when market participants implicitly price the reinvestment period in excess of the complex reality they can forecast. As the recent case of Kraft Heinz demonstrated, there may be broad market misconceptions about the durability of reinvestment opportunity in some of these business models. Valuations in stocks like Roper, Danaher, Constellation Software may already broadly reflect these biases, potentially subject to limited addressable markets and eroding business moats.

Structural change which is discontinuous with past history: Any strategy using historical data-sets would have a hard time participating in these opportunities. DeepMind AI recently beat top-ranked human players at a complex real-time strategy game called Starcraft. Structural change is the equivalent of making a computer play a combination of Starcraft + World of Warcraft. A human, such as a generalist, who trades across sectors, might have some intuition around this – a computer, at least for awhile, would be completely lost.

Bets in complexity are of course hard, but it all depends on the prices available. Luckily today’s technology-disruption provides abundant fodder: this was the somewhat hidden point of the last essay, Mapping Emerging Scarcity. It could be the preserve of a few extraordinary managers or it could be the preserve of the expert-generalist: with so much of the investment world organized around sector-silos, this might be an area where a minority can front-run underlying changes.

These insights require real skill and are perhaps not scalable across an organization: good process can be taught, complex intuition is a bit trickier. But that’s what successful investing is: we are paid to see emergent change using all the creative facilities still available to the human mind. And the most successful investors are not those who succeed within a single regime, like the tribe of the value investor, but those investors who are successful across regimes, like Seth Klarman, Andy Beal, Richard Rainwater, and Steve Cohen (moving from options / merger arb, to generalist fundamental L/S, to sector-specialist L/S, to quant-data high frequency?). And make no mistake, today’s investment eco-system is moving across regimes, as "the water investors swim in" changes.

Thanks to J.S., K.P., and E.S. who provided thoughts and comments. Special credit to M.B. & G.S. who led me to recognize the market as a “special situations” habitat. To T.T. who helped me recognize the price-inefficiencies in compounders. And to S.Y., with his story of the disappearing London-based Japanese warrant traders, and their HP option calculators, who probably recognized earlier than most, that we are all playing the investing meta-game, or the game within the game.